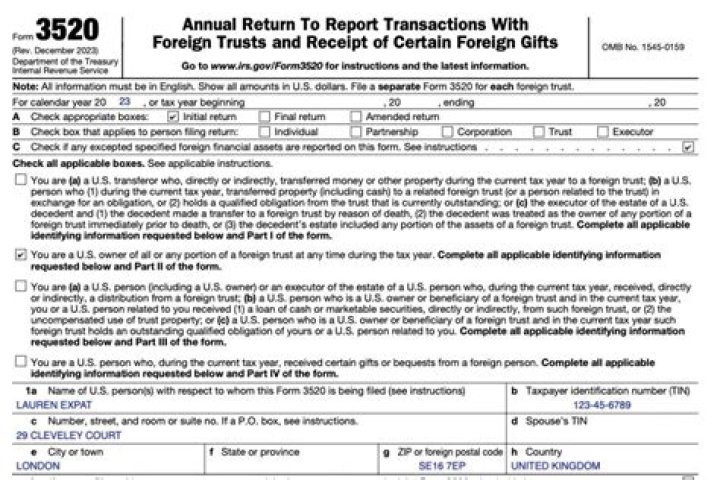

If you are a U.S. person (other than an organization described in section 501(c) and exempt from tax under section 501(a)) who received large gifts or bequests from a foreign person, you may need to complete Part IV of Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign …

Who Must File form 3520a?

trustee

The trustee of a foreign grantor trust with a U.S. grantor must complete an annual Form 3520-A, which is substantially like the income tax return of a U.S. trust. If the foreign trustee will not complete the return, it is the duty of the U.S. grantor to prepare and file the return.

What is the difference between form 3520 and 3520-A?

Generally, Form 3520 is a filing required of the recipient of foreign assets, and Form 3520-A is an additional, less commonly required form that is submitted by a trustee when there are beneficiaries or owners of the trust that are U.S. taxpayers.

What is the purpose of form 3520?

The Form 3520 is an informational return used to report certain transactions with foreign trusts, ownership of foreign trusts, or large gifts from certain foreign persons to the Internal Revenue Service (“IRS”).

What happens if you don’t file Form 3520?

The penalty for failure to file a Form 3520 reporting a foreign gift or bequest, or for filing an incorrect or incomplete form with respect to a gift or bequest, is 5% of the gift or bequest for each month during which the failure continues, up to a maximum of 25% [IRC section 6039F(c)(1)(B)].

Is Form 3520 filed separately or with 1040?

Form 3520 Filed Separately The form 3520 as filed separately from your income tax return. As provided by the IRS: “In general, the due date for a U.S. person to file a Form 3520 is the 15th day of the 4th month following the end of the U.S. person’s tax year.

What is a 3520-A?

Form 3520-A is the annual information return of a foreign trust with at least one U.S. owner. The form provides information about the foreign trust, its U.S. beneficiaries, and any U.S. person who is treated as an owner of any portion of the foreign trust under the grantor trust rules (sections 671 through 679).

What do I attach to Form 3520?

U.S. persons (and executors of estates of U.S. decedents) file Form 3520 with the Internal Revenue Service (IRS) to report:

- Certain transactions with foreign trusts,

- Ownership of foreign trusts under the rules of sections 671 through 679, and.

- Receipt of certain large gifts or bequests from certain foreign persons.

What is a form 3520?

U.S. persons (and executors of estates of U.S. decedents) file Form 3520 with the Internal Revenue Service (IRS) to report: Certain transactions with foreign trusts, Ownership of foreign trusts under the rules of sections 671 through 679, and. Receipt of certain large gifts or bequests from certain foreign persons.

Can I file Form 3520 electronically?

While Form 3520 must be printed and paper filed, by mail (it cannot be e-filed), there is no reason that this should interfere with your regular income tax return preparation and filing.

What is the failure to file penalty for Form 3520-A?

The IRS requires a U.S. person receiving a gift from a foreign individual, corporation, partnership, or estate to report by filing Part IV Form 3520. Failure to file or late, incorrect, or incomplete filing is subject to a severe penalty. A penalty of 5% of the amount of the gift for each month not reported is given.

How do I submit Form 3520?

Send Form 3520 to the Internal Revenue Service Center, P.O. Box 409101, Ogden, UT 84409. Form 3520 must have all required attachments to be considered complete.