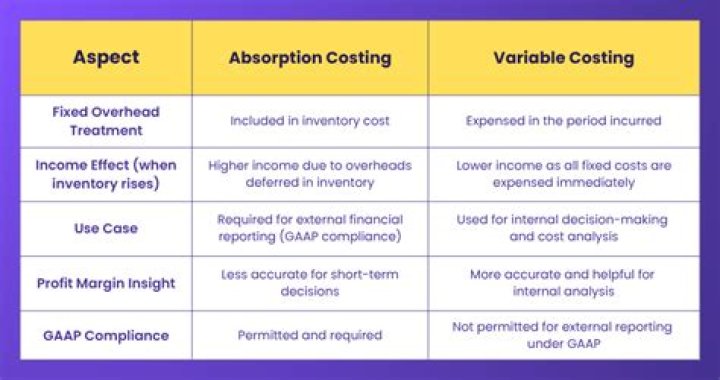

The net operating income under absorption costing systems is always higher than variable costing system when inventory increases during the period. The net operating income under variable costing systems is always higher than absorption costing system when inventory decreases during the period.

Is absorption costing on the income statement?

The traditional income statement, also called absorption costing income statement, uses absorption costing to create the income statement. This income statement looks at costs by dividing costs into product and period costs.

What explains the difference between operating income computed using absorption costing and operating income computed using variable costing?

What factor is the cause of the difference between operating income computed using absorption costing and operating income computed using variable costing? a. Absorption costing considers all manufacturing costs in the determination of operating income, whereas variable costing considers only prime costs.

What is variable costing income statement?

A variable costing income statement is one in which all variable expenses are deducted from revenue to arrive at a separately-stated contribution margin, from which all fixed expenses are then subtracted to arrive at the net profit or loss for the period.

Is variable costing the same as marginal costing?

Marginal costs are a function of the total cost of production, which includes fixed and variable costs. By contrast, a variable cost is one that changes based on production output and costs.

When reviewing the differences between variable costing and absorption costing the primary difference is?

The difference is that the absorption cost method includes fixed overhead as part of the cost of goods sold, while the variable cost method includes it as an administrative cost, as shown in Figure 6.12.

What is a key difference between absorption costing and marginal costing?

In summary The key differences between marginal and absorption costing are: Purpose – marginal costing enables well informed short-term decision making, and absorption costing calculates the cost of output as well as providing the closing inventory valuation for inclusion in the financial statements.