Overview. You must pay Class 1A National Insurance contributions on work benefits you give to your employees, such as a company mobile phone. You must also pay them on payments of more than £30,000 that you make to employees when their employment ends, such as a redundancy payment (‘termination awards’).

What reference do I use when paying P11D?

Reference number You’ll need to give a 17-character number as the payment reference. This starts with your 13-character Accounts Office reference number. Then add the tax year you want to pay for and the digits ’13’ to make sure your payment is assigned correctly.

How do I report a Class 1A NIC?

Report the Class 1A NICs due:

- complete the Class 1A NICs declaration on form P11D(b), using the amount from Step 2.

- return the P11D(b) together with completed P11Ds by 6 July.

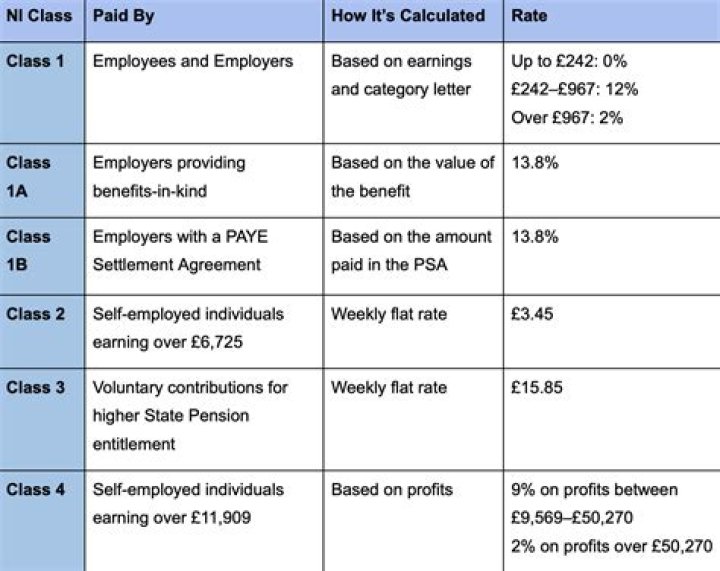

What is the difference between Class 1 and Class 1A NIC?

Class 1 National Insurance contributions (NICs) are payable by employees and employers. Employed earners (employees) pay primary contributions and employers pay secondary contributions. Employers are also liable to pay employer-only Class 1A NICs on most taxable benefits and expenses.

Do employees pay Class 1A NIC?

Class 1A NICs are paid by employers only. There’s no employee contribution payable.

What is the Class 1A NIC rate?

13.8%

The percentage rate at which Class 1A National Insurance contributions are worked out is the employers’ Class 1 National Insurance contributions rate for the tax year in which the benefit is made available. For the tax year 2020 to 2021, the Class 1A percentage rate is 13.8%.

Is Class 1A NIC tax deductible?

A payment of Class 1A NIC is deductible from the employer’s taxable profits. if no such contribution is payable, the person who would be liable to pay employer’s Class 1 NIC, if the benefit itself had been earnings on which Class 1 NIC is due (SSCBA 1992, s.

What class of Ni do employees pay?

Employees. Employees pay Class 1 national insurance contributions of 12% on earnings above the £184 per week primary threshold. You will only pay contributions of 2% on any earnings over £967 per week. If your income falls below the primary threshold, you will not need to pay any contributions.

How much is Class 1 National Insurance?

Employers are also expected to pay Class 1 NICs (known as secondary contributions) at 13.8% on the earnings of each employee who earns more than the primary threshold. This contributes, among other things, towards the employee’s entitlement to statutory payments.

What happens if my employer doesn’t pay my National Insurance?

Employers will deduct tax and National Insurance from the wages they pay out. If you are concerned that your employer may not be paying your National Insurance Contributions to HMRC, a low-key way of checking that your contributions are getting through would be to ask for a pension forecast from the Pensions Service.

Is Class 1A NIC an allowable expense?

Exempt from Income Tax Class 1A NICs are payable only where the benefit provided is chargeable to Income Tax under ITEPA 2003 on an amount of general earnings as defined at Section 7(3) ITEPA 2003.

What is the correct Nic payment reference for Class 1A?

I have always advised clients that when they pay their Class 1A NIC that the payment reference is their 13 digit Accounts Office reference plus 4 digits (i.e. 18-19 would be 1913). I’ve never had any issues in the past.

What are Class 1A National Insurance Contributions ( NICs)?

Class 1A National Insurance contributions ( NICs) are payable on most benefits provided to employees. This guide tells you what you need to know about Class 1A NICs. It explains when Class 1A NICs are due and how they’re worked out, reported and paid. Paragraphs 4 to 26 explain the general rules about Class 1A NICs.

Do I have to pay Class 1A National Insurance on termination Awards?

You only have to pay Class 1A National Insurance contributions on termination awards if you have not already paid Class 1 National Insurance contributions on them. There’s different guidance on payment of Class 1A National Insurance on sporting testimonials.

How are Class 1A NICs calculated for salary sacrifice?

Where a benefit is provided as part of salary sacrifice or other optional remuneration arrangement ( OpRA ), special rules apply and the Class 1A NICs are calculated as a percentage of the relevant amount. Further guidance is provided in booklet 480: Expenses and benefits – a tax guide. Certain conditions must apply before Class 1A NICs are due.