The calculation itself is relatively simple. First, multiply the average accounts receivable by the number of days in the period. Divide the sum by the net credit sales. The resulting number is the average number of days it takes you to collect an account.

How do you calculate days sales in receivables ratio?

The ratio is calculated by dividing the ending accounts receivable by the total credit sales for the period and multiplying it by the number of days in the period. Most often this ratio is calculated at year-end and multiplied by 365 days. Accounts receivable can be found on the year-end balance sheet.

How do you calculate accounts receivable turnover in days?

The accounts receivable turnover ratio formula is as follows:

- Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable.

- Receivable turnover in days = 365 / Receivable turnover ratio.

- Receivable turnover in days = 365 / 7.2 = 50.69.

How do you calculate average days collection ratio?

It is calculated by dividing receivables by total sales and multiplying the product by 365 (days in the period). To determine whether or not your average collection period results are good, simply compare your average against the credit terms you offer your clients.

How do you calculate collection period?

How Is the Average Collection Period Calculated? The average collection period is calculated by dividing the average balance of accounts receivable by total net credit sales for the period and multiplying the quotient by the number of days in the period.

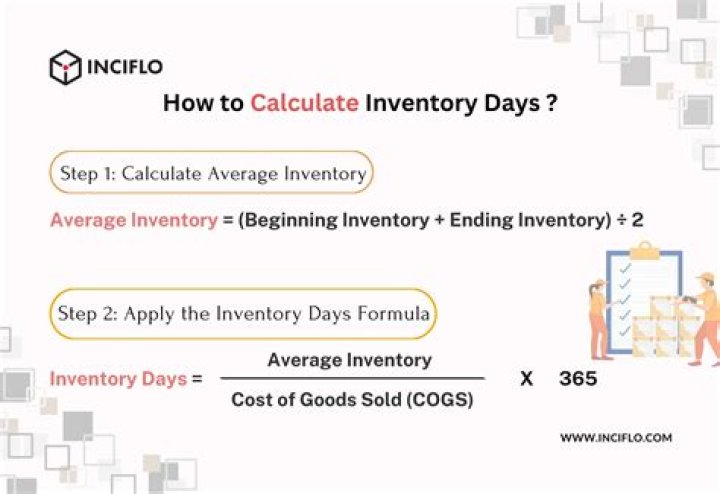

How do you calculate days in hand inventory?

You can calculate your inventory days on hand with this formula:

- Average Inventory/(Cost of Goods Sold/# days in your accounting period) = Inventory Days on Hand.

- (Beginning Inventory + Ending Inventory) / 2 = Average Inventory.

- # days in your accounting period/Inventory Turnover Ratio = Inventory Days on Hand.