A NOL is first used to offset income in the year of the NOL, but if the NOL exceeds 80% of the income, then it can be used to offset income in future years. However, a NOL carryforward does not reduce income subject to self-employment tax; only income subject to the marginal tax is reduced.

Can an AMT NOL be carried back?

Yes, if the MTC generated or released by the NOL carryback in one year in the carryback period is used in a subsequent year in the carryback period to reduce the C corporation’s tax liability (as opposed to resulting in a refundable MTC), then the C corporation may claim a refund for any decrease in tax resulting from …

Does NOL offset taxable income?

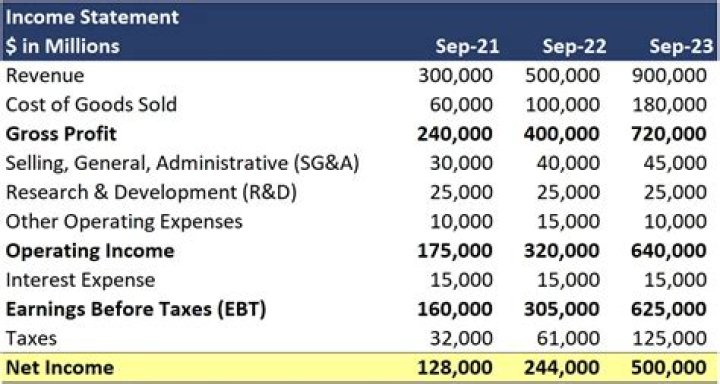

NOL Carryforward Example The carryover limit of 80% of $6 million is $4.8 million. The full loss from the first year can be carried forward on the balance sheet to the second year as a deferred tax asset.

What is considered non business income for NOL?

For purposes of section 172, nonbusiness deductions and income are those deductions and that income which are not attributable to, or derived from, a taxpayer’s trade or business. Wages and salary constitute income attributable to the taxpayer’s trade or business for such purposes.

Can business losses offset personal income?

Generally, business losses that are passed through to these owners can be used to offset other personal income. But if there is an excess business loss, it can’t be used currently. Instead, it’s treated as a net operating loss (NOL) carryover.

What is the difference between NOL and AMT NOL?

A net operating loss (NOL) is defined as a taxpayer’s excess deductions over a taxpayer’s gross income. Similarly, AMT NOL is defined as deductions defined by alternative minimum tax rules over alternative minimum tax income (AMTI).

How does NOL affect AMT?

A net operating loss (NOL) is a loss taken in a period where a company’s allowable tax deductions are greater than its taxable income. The amount of ATNOL that can be deducted when calculating AMT income cannot exceed 80% of the obligation.

Can a sole proprietorship loss create an NOL?

Sole proprietorship can use NOLs to reduce taxes in other years. If you have a net operating loss from your sole proprietorship, you’ll normally be able to deduct the loss from your total income from other business ventures or from any salary, wages, or other earnings.

What is non business income?

Nonbusiness income means all income other than business income and may include, but is not limited to, compensation, rents and royalties from real or tangible personal property, capital gains, interest, dividends and distributions, patent or copyright royalties, or lottery winnings, prizes, and awards.